THE PAGE NEVER TURNED

New Year. Same Story

Every January we pretend the calendar did something magical—fresh starts, clean slates, new resolutions. But ready or not, life keeps barreling forward: fast, noisy, and indifferent.

So far, 2026 has wasted no time proving that point. January so far has been…chaotic, to say the least. That holiday reset—followed by the return to “reality”—emphasized why it was needed in the first place. No matter where you turn—markets, geopolitics, technology, cannabis, culture—the calendar flip blasted a screeching alarm that this era of transformational change never went on vacation.

Do you feel it?

For the first Sesh of the year, I’ll level-set where we left off and where I think we’re going. As always, I’ll write from the vantage point I know best: an investor and operator living inside transformational change, not theorizing about it from the sidelines. True to form, my views are filtered through the lens I trust—usually about a half-gram into my Zig-Zag.

First, I’ll update drivers behind the Safety, Spiffs & Stupidity framework—my “north star” to navigate and monetize these transformations. For market-focused paying subs, I’ll show you how I’m positioned in my “active” portfolio.

Next, I’ll revisit cannabis through this broader lens. I’ll cover any changes to my thesis and positioning based on what I’m seeing in real time, on the ground. To beat a dead horse, you can’t understand cannabis unless you understand the consumer. And you can’t understand the consumer unless you understand how s/he fits within the broader transformations at play.

This year, Sunday Sesh evolves. Expect more experimentation. More engagement. More perspectives. I’ll also further detail how I’m actually harnessing these transformations—like AI—inside the boardroom and at home. If nothing else, it may help assuage fears that all this attention is pointless. (Spoiler: it’s not)

So with that, roll up a fat doink and let’s dive in.

Welcome to Sunday Sesh 2026.

2/NEW YEAR, SAME STORY

About 18 months ago, the early Safety, Spiffs & Stupidity framework made it from my brain to the journal for its eventual public launch last year. At that time I could feel multiple transformations gathering kinetic energy, stacking on top of one another, and swiftly moving towards a collision. I created this framework not only as a way to allocate capital, but just as importantly, to navigate life with the right mindset to prepare for what’s coming.

Almost a year to the day, I laid out two conclusions that remain central to this framework:

Humans Simply Can’t Think Exponentially: Most won’t put in the work to understand why. And by extension, most won’t understand why certain companies will dramatically compound because their lens is too damn short. This year, I truly believe we won’t be able to know if we’re “looking up or down” as our noses are pressed against the vertical line. Expect constant paranoia and euphoria to co-exist, and the pendulum will likely swing hard and without warning. Today’s software/SAAS implosion vs. hardware/chips is a great illustration.

Know What You Own: It’s still a great time to be an active investor to weave and bob across the market’s structural, fundamental, and behavioral constraints. Everyone has an edge. Use it.

3/SAFETY, SPIFFS & STUPIDITY: A FRAMEWORK

Like you, I’m eagerly trying to monetize these transformations right in front of us, while staying mindful of the incredible risks as we transition.

While the actual components of the portfolio will constantly change, let me stress again I’m designing a “synthetic convert” that carries mispriced convexity:

SAFETY: Create a (near) risk-free bond floor that’s kicking off durable yield, now with risk-free rates firmly off zero (even if they inevitably go there again);

SPIFFS: Use some/all of that yield to buy highly attractive and asymmetric payoffs; and

STUPIDITY: Neuter (some/all) beta with thematic and company-specific long/shorts in my zones of competency.

The goal isn’t to avoid risk; it’s to reframe it—to separate perceived danger from actual fragility, and to structure exposure so I can stay in the trade without blowing myself up.

4/WHY DOES THIS OPPORTUNITY EXIST

All three attractive opportunity sets—SAFETY, SPIFFS & STUPIDITY—exist for three main reasons that feed on each other:

Structurally — Machines, Mandates, and Mismatched Capital

Over 70% of market activity is no longer “human.” Capital is deployed by systems designed to hug benchmarks, minimize tracking error, and avoid career risk. The result is forced concentration and crowd-like behavior that looks stable—until it isn’t.

When conditions shift, these structures unwind violently, leaving large wakes and persistent imbalances.

Layered on top of this are professional constraints. Pod PMs operate with leverage, narrow sector mandates, and constant pressure to stay fully invested. They don’t ask whether a sector is attractive—only how to allocate within it.

On the other end, many long/short generalists lack capital duration, leaving them with assets that need time to season but liabilities that don’t allow it. Structural fragility is baked in.

Fundamentally— Speed Beats Process

The world is accelerating faster than traditional Wall Street workflows can handle. By the time most professionals complete their underwriting, the alpha has already been harvested by faster, more flexible capital.

It’s not a lack of intelligence—it’s a lack of speed and willingness to operate outside rigid process. The market increasingly rewards those who can do the work quickly and act decisively, not those who wait for perfect information.

Behaviorally — Humans Misprice Convexity

The humans still involved in price-setting tend to be emotional, nihilistic, inexperienced—or all three. This cohort gravitates toward “left-for-dead” companies, particularly below $5-10 BN in market cap.

As a result, convexity—the non-linear response of price to incremental changes in fundamentals or policy—is routinely mispriced. Implied volatility remains muted until fundamentals inflect or fresh capital arrives, at which point realized volatility overwhelms models.

Cannabis is a textbook example. Expect more of this behavior in 2026.

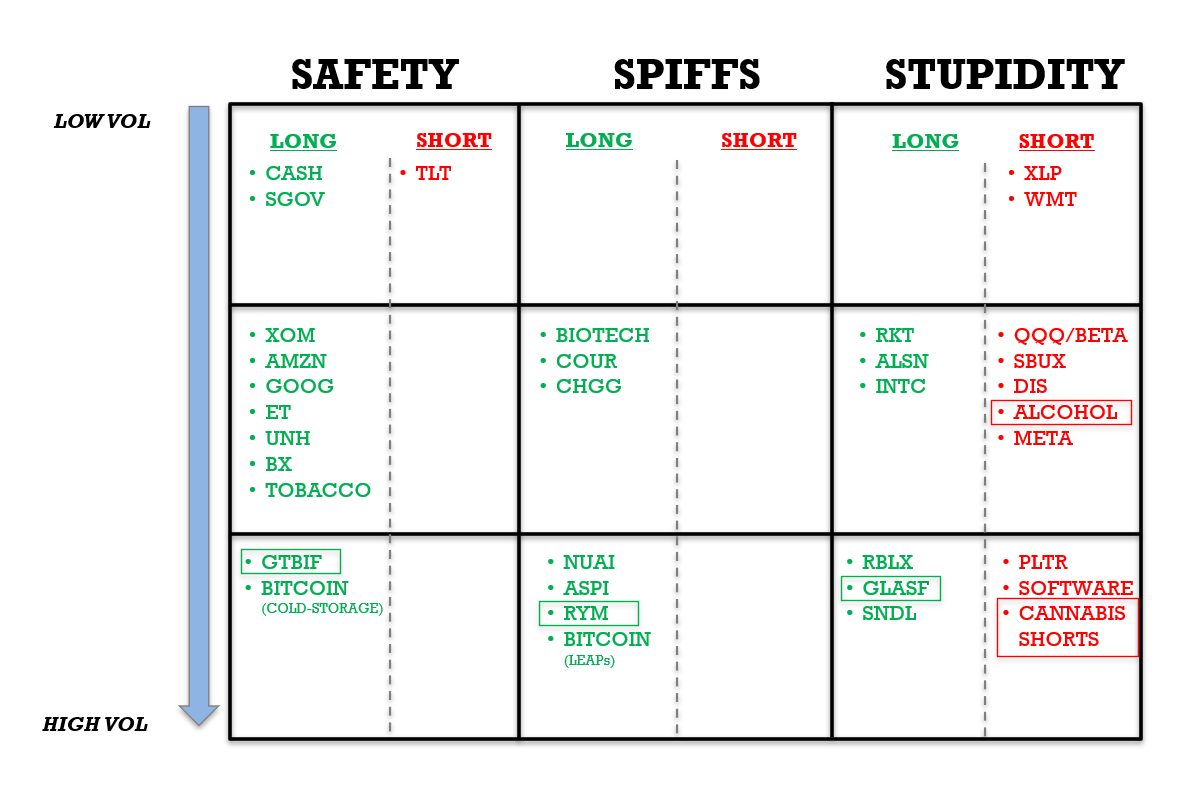

5/DRUM ROLL PLEASE

Over the past year it was very clear there’s a strong cohort inside the Sesh that only wants my “stonk” picks. To be very clear, Sunday Sesh will NOT be Seeking Alpha. And also to be very clear—my problems aren’t necessarily your problems—and therefore how I approach portfolio construction may not be right for you. As always, I’m here to give you the tools so you can replicate based on your own edge and situation.

With that said, below is a rough idea of my active portfolio…and given what’s happened so far in 2026 it continues to meaningfully outperform. It might not in the future.

Last Sesh I called out that i was carrying more “safety” into year end—largely to take profits after a very healthy year of outperformance, and largely to take some necessary time to get away from it all. But I keep buying Bitcoin every day (I’m not joking).

For cannabis, see the green and red boxes. Yes, there are some below that are hidden, like my cannabis shorts and select biotech names which I won’t disclose.

You do you. Know what you own.

6/WEED WEIGHT

A few detailed call-outs on above:

Cannabis — Same horses as Q4. I added materially to Glass House in Q4 (as subs saw) and remain long GTI, though I expect FY’26 guidance to be noisy as RYM royalties get carved out—so make room for confusion. Bigger today than a year ago, but I’m still not at full size. Be a liquidity provider, always. From my seat, nothing has changed—except price.

On the ground, I continue to believe 2026 brings incremental reform (S3), broader state adoption, and—most importantly—stronger consumer demand driven by new markets, alcohol substitution, and hemp switchers. Open your eyes: cannabis has clearly moved into the cultural mainstream. It’s becoming almost…normal.

The familiar themes remain intact. Bifurcation. The strong get stronger. The TAM may look stagnant on paper, but volume growth is being masked by maturing prices. Scale and operational skill are still underappreciated assets for the best-run operators—and those advantages will increasingly offset perceived revenue pressure. Growth could easily surprise to the upside against today’s low expectations, especially in markets where pricing has stabilized (which is exactly what happened in Canada).

Post-S3, free cash flow is likely not going to capex or price wars—at least not yet. It’s likely headed into opex, balance sheet repair, and selective tuck-in M&A. Distressed players will either disappear or go private. Hemp enforcement is real, and I’m seeing tightening supply across multiple markets as bad actors—especially in vape—exit. Consumers are getting smarter too, which will further bifurcate shelves around quality and repeat behavior.

From a valuation standpoint, the bifurcated potential winners remain very cheap at roughly ~5-6x LTM EBITDA versus where these businesses should trade over a 1–5 year horizon. Some names—GTI specifically—are relatively safe, with very low leverage and real cash generation (which just amplifies how cheap the equity is). Glass House doesn’t look cheap on paper, but has embedded formulaic growth that outstrips the entire sector (imho). Structurally, the Street still appears to be short gamma in a market with liquidity the size of a mouse hole—making this a perpetual ticking bomb and keeping convexity mispriced.

With a “free look” into Q4 earnings and 2026 guidance in late February, it’ll be an interesting 4-6 weeks. My finger is on the trigger for spiffier exposure if investor boredom sets in. Demand leads policy. Always.

Big Alcohol: Still slightly short, but I massively harvested the 3+ year short. Most of these names have underperformed the S&P by 50% over the past ~3 years so it’s been a home-run bet. Doesn’t mean I won’t revisit the short, but there are a few names that are getting cheap as capacity gets sucked out of the system despite the frightening inventory build that will take years to blow off. Longs won’t work yet, but I can see them outperforming beta and possibly Big Food (another sector I’m negative on, but just not so short anymore).

QQQ / Software–Yes, I’m short and have been since late November. And since I’m long a few—AMZN, GOOG—this is just a reflection that I think beta and risk premium are rather stretched. I have no interest being longer the Mag7 which is 40% of the index. And it wouldn’t surprise me if these names lagged all year. On software, I’m looking to get long…somewhere. It strikes me that everything is being tossed indiscriminately, which is starting to reveal many very “sticky” businesses with incredible data moats. So I’m looking to catch some high-quality knives in software this year. None yet. MNDY is on my short list.

7/MACRO BACKDROP

We’re operating in a market where beta is increasingly fragile, growth is being pulled forward by policy and national-security-driven investments, and humans are struggling to process exponential change. Inflation in the things that matter—energy, housing, healthcare, metals, and other hard assets—remains structurally sticky even as technology deflates information and services. That mix creates violent dislocations, frequent narrative breaks, and persistent mispricing of convexity—making passive exposure dangerous and active construction essential.

I’ll unpack these dynamics in more detail in upcoming Seshes.

Hope this helps. Here’s to a successful 2026.

Onward,

SUNDAY SESH

***Disclaimer: Not financial or investment advice, do your own work; this is intended for sophisticated investors. No conflicts, no MNPI, these are my own opinions, and no representation that what’s presented is accurate. As disclosed, authors of SUNDAY SESH hold common shares and derivatives of companies mentioned and they have no obligation to update or disclose changes. No representation is made as to accuracy or completeness. Past performance is not indicative of future results. And as always, cannabis was used frequently in the authorship to creatively solve problems.

The TLT short is interesting… bear steepener trade?