TIME COMPRESSION

Duration, Convexity, and the New Structure of Volatility

One of the benefits of getting older in this game is that you accumulate scar tissue. Markets have a way of humbling you if you stick around long enough. And if you’re lucky, you develop something even more valuable: perspective.

At the depths of the Great Financial Crisis the VIX spiked into the high 80s. The market’s fear gauge was screaming for its mommy. On top of managing the portfolio, my team and I were modeling scenarios early Sunday mornings around which banks might not open the next day. Regularly.

It felt like the entire system was burning down.

I remember those feelings viscerally and can recreate them instantly—the good and the bad. All of it still sits just below the surface. In fact, I spend a lot of energy making sure my mind doesn’t go back there too often.

Experiences like that leave a mark. They armor investors. They teach humility. And they recalibrate your sense of how markets behave when things break.

But what’s interesting is what happened next. From the end of the GFC through much of the following decade, volatility steadily declined. Central banks flooded the system with liquidity, interest rates collapsed, and risk premiums compressed across the entire capital structure. Looking back, markets entered one of the most stable financial regimes in modern history.

And for folks like me, we adapted but never forgot.

By 2017, the VIX briefly touched 10. Ten! The markets barely moved. Although the global economy was growing in unison, chaos was everywhere. Hurricanes and wildfires. North Korea firing missiles. The #MeToo movement reshaping culture. Trump nuking political norms. Yes, I keep receipts.

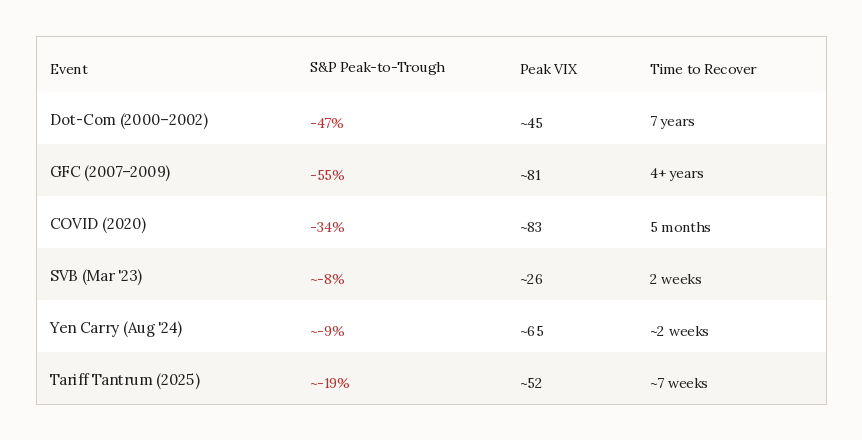

Looking back, that calm likely marked the beginning of a regime shift. Since then, while volatility is still relatively muted, we see these recurring sharp intermittent spikes reminding investors how fragile the system can be. Volmageddon in 2018. COVID in 2020—sending the VIX to 83, its 2nd highest reading. Then SVB in March 2023. The yen carry unwind in August 2024. And finally, the Tariff Tantrum last year. Today with the VIX hovering around 30, it seems we might be on the verge of another.

Different catalysts, same message: markets can flip on a dime. And in both directions.

Diving deeper, the more interesting observation isn’t the spikes themselves, but rather how the market processes these shocks faster than it used to. Look at the trajectory—and the severity—of major drawdowns since the DotCom bubble:

Dot-com dragged on for years. The GFC took more than a year to bottom. COVID fell ~35% in a month—then snapped back as liquidity arrived. Since then, panics hit hard but resolve relatively quickly usually in a matter of weeks or months.

That’s not just volatility.

That’s time compression.

I’ve been hammering this theme for months as our world rapidly transforms. Something bigger—something structural—is likely happening.

I’m going to dive into the weeds on why: i) Time Compression; ii) Mispriced Convexity; and iii) Mechanical Capital.

Themes I’ve uncovered before, but now through the lens of volatility. Once you start viewing markets through that lens, these moves we’ve seen over the past few years stop looking like anomalies. They start looking like features of a faster system.

So let’s roll a big boy joint and let’s get volatile. There’s enough to go around—this SESH is on me (read: FREE). If you’re new here, spend time with the backlinks—and if you can’t, have your agent do it.

Welcome to SUNDAY SESH.

1/ AI IS COMPRESSING TIME

Historically, markets priced risk around predictable rhythms. Earnings cycles. Fed meetings. Quarterly guidance. Analyst revisions. Information moved in waves where investors had time to process and debate developments. Price discovery was messy, but it was gradual.

That cadence worked because the underlying pace of change was relatively slow, which aligned with the financial architecture built for a slower world. A world where “long duration” meant the future was far away and uncertainty could be discounted gradually.

For most of the past decade investors weren’t just buying earnings. They were buying time. Time before meaningful competition arrived. Time protected by scale, distribution, switching costs, and capital intensity. Think back to prior SESHES—like CONTENT IS NOT KING—to understand how time was a sharp weapon that’s now blunted.

In this old era, time was the moat. And if the Internet chipped away at that moat, AI simply obliterated it.

Why? Technology—specifically AI—compresses time. Today, a model release can reprice an entire sector in days as investors rethink the economics of incumbency. We saw this in software in Q1, and the shock spilled into insurance and logistics—anywhere automation or cost curves can shift quickly. Today the future arrives all at once.

When the replacement cost of competence collapses—when code can be generated instantly and iterated continuously—competitive cycles shrink. A product that once enjoyed years of defensibility may now face viable competition in months.

The point isn’t whether those moves were right or wrong. The point is how fast they happened.

Markets aren’t mispricing companies.

They’re mispricing speed.

And when speed becomes the dominant variable, volatility changes character. In this new compressed system, information flows instantly and capital reacts mechanically.

Price discovery no longer happens smoothly—it happens in bursts.

2/DURATION: CAP STRUCTURE TENSION

Once you start looking at markets through that lens, you begin to see interesting tensions emerge across the capital structure. Specifically, debt and equity need fundamentally different things to function properly.

As we say: debt is built on reality, equity is built on hope. I should know—I’ve been lucky to invest in both, and frequently at the same time.

Debt needs certainty. Predictable, stable cash flows. Healthy coverage ratios. LTV cushions. Whether you’re underwriting mortgages or software private credit, the premise is the same: you’re betting that the future will resemble the past.

Equity is different. Equity is priced off the riskiness of that credit, and by extension, what risk premium equity investors demand. The upside lives in uncertainty—the possibility that value can compound with unlimited return.

But AI complicates both sides of that equation.

If technological change accelerates dramatically, long-duration assumptions become harder to model. And if you can’t confidently model what a business looks like in the future, pricing the spread between debt and equity becomes unstable. Some argue it might even collapse on itself.

That’s why you get “freak-outs” across the capital structure. Sometimes it shows up in debt —like SVB, where duration risk suddenly mattered again. Or today’s private credit. And sometimes it shows up in equity—COVID, tariffs, the violent software repricing.

In both situations, a lack of capital structure fluency and the inability of pros to color outside the lines causes enormous confusion. But the underlying tension is the same.

The system is struggling to price duration.

3/MISPRICED CONVEXITY

Putting #1 and #2 together leads to another critical factor I talk about a lot: mispriced convexity.

Not textbook convexity. What I’m referring to is structural convexity—the kind created by incentives, positioning, and narrative risk.

In this context, convexity means securities behave like loaded springs. They can sit dormant for long periods of time, building tension beneath the surface, until something shifts and the price moves violently.

Professional investors aren’t paid to be early, and they certainly aren’t paid to be the last one out. So capital tends to cluster around consensus trades until suddenly it doesn’t. When positioning becomes crowded, markets become fragile. (See: BETA SCARES THE FUCK OUT OF ME.)

The result is what traders call “air pockets” where the leading narrative holds everything together until it cracks. And once it does, it simply snaps—often in both directions.

Convexity cuts both ways. While most investors focus on explosive moves higher, we’ve seen plenty on the downside as well. Banks during SVB, UnitedHealth last year, and software this year are a few that come to mind.

Violent moves. Sudden factor unwinds. Massive deleveraging on the way down, and almost chase-like behavior on the way up.

The magnitude of those moves isn’t new.

The speed is.

4/YOU ARE NOT HUMAN

Finally, there’s another layer to this thesis that investors often underestimate: the marginal investor today is increasingly non-human.

ETFs. Robo-advisors. Quants. Fixed-allocation strategies. Risk parity. Trend followers. Now add in AI, and the list goes on and on.

By some estimates, more than 80% of market activity is no longer human. Capital is deployed by systems designed to hug benchmarks, minimize tracking error, and avoid career risk. The result is forced concentration and crowd-like behavior that can appear stable for long periods of time—until it suddenly isn’t.

From experience, what I see is that machines, their mandates, and their mismatched capital now dominate the system. These “mechanical” investors don’t operate the way discretionary investors do. They may have conviction in their frameworks, but from a security-selection standpoint they don’t really care what’s inside the portfolio.

They care about the scaffolding, not the bricks.

Similarly, the remaining human pros amplify this system. These narrow sector pods operate with enormous leverage and are under constant pressure to stay fully invested. They don’t ask whether a sector is attractive—they simply are forced to allocate within it. (Insane if you ask me, which I repeat constantly to close friends who are some of the best pod PMs in the world.)

And because everyone operates similarly, their collective behavior is defined by triggers. Volatility thresholds. Drawdown limits. Momentum signals. Factor controls. Covariance matrixes.

When those triggers fire, the response is mechanical. Positions are cut. Leverage is reduced. Exposure is rebalanced. The dial is turned down.

And because so many of these strategies rely on similar signals, they tend to move at the same time.

The result: a system where repricing happens instantly. Can you feel it?

5/THE FUTURE PIVOT

With the VIX today around ~30, we’re probably nowhere close to peak fear. That said, we’re just about the area where the market starts looking for a pivot.

Historically, that pivot almost always comes in the form of more liquidity. Whether it’s bailing out the banks and credit during GFC and SVB, or bailing out the equity during COVID and the Tariff Tantrum—it always comes back to more liquidity in the system.

This time—however—it’s murky.

My base case is that the system resolves itself the same way it always has. Wars and geopolitical shocks are expensive. Worse, Middle America—the administration’s main audience—is about to get its balls squeezed in ways markets may not fully appreciate yet as oil screams higher.

And when the bill comes due, the easiest way for policymakers to stabilize the system is the same lever they’ve been pulling for the past fifteen years. PRINT MOAR FIAT.

My view is that the next round of liquidity simply might not look and feel the same way—whether it’s UBI, or cost curve controls, or AI bailouts. Which in my mind is a matter of when, not if.

6/LET’S BRING IT HOME

I certainly don’t know what tomorrow brings, but I’m highly confident in a few key themes that sit in the background as I deeply focus on specific-company transformations over a defined duration. Which in some cases, is forever.

So to wrap up this SESH, here my key take-aways:

Time is compressing, fueled by transformational AI;

Convexity is mispriced, exacerbated by capital structure convergence;

Market structure is increasingly non-human, forcing mechanical shifts; and finally

Liquidity always arrives, until it doesn’t.

Hard to tell where we end up. For you and me, just focus on buying right. And if you must hedge, hedge stupidity.

Onward,

SUNDAY SESH